The war in Ukraine has caused major supply disruptions and led to historically higher prices for a number of commodities. For most commodities, prices are expected to be significantly higher in 2022 than in 2021 and to remain high in the medium term. The price of Brent crude oil is projected to average $100/bbl in 2022, a 42 percent increase from 2021 and its highest level since 2013. Non-energy prices are expected to rise by about 20 percent in 2022, with the largest increases in commodities where Russia or Ukraine are key exporters. Wheat prices, in particular, are forecast to increase by more than 40 percent this year, reaching an all-time high in nominal terms. While prices generally are expected to peak in 2022, they are to remain much higher than previously forecast. The outlook for commodity markets depends heavily on the duration of the war in Ukraine and the severity of disruptions to commodity flows, with a key risk that commodity prices could be higher for longer. A Special Focus section investigates the impact of the war on commodity markets and compares the current episode with previous price hikes. It finds that previous oil price hikes led to the emergence of new sources of supply and reduced demand through efficiency improvements and substitution of other commodities. In the case of food price hikes, additional land came into use for production. For policymakers, a short-term priority is to provide targeted support to poorer households facing higher food and energy prices. Over the longer term, they can encourage energy efficiency improvements, facilitate investment in new sources of zero-carbon energy, and promote more efficient food production. Recently, however, policy responses have tended to favor trade restrictions, price controls, and subsidies, which are likely to exacerbate shortages.

Recent trends

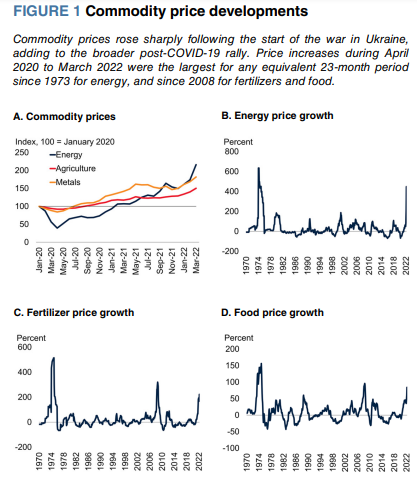

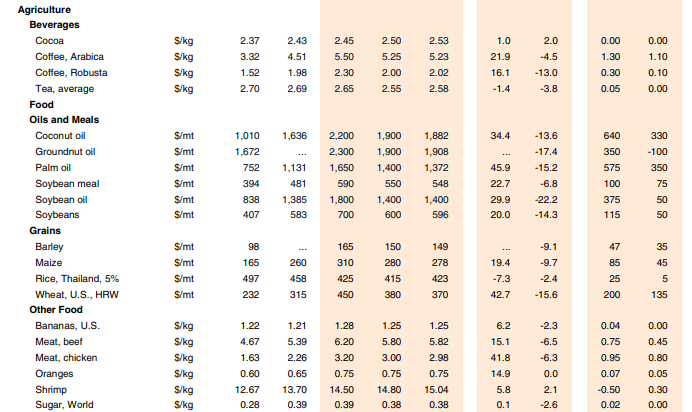

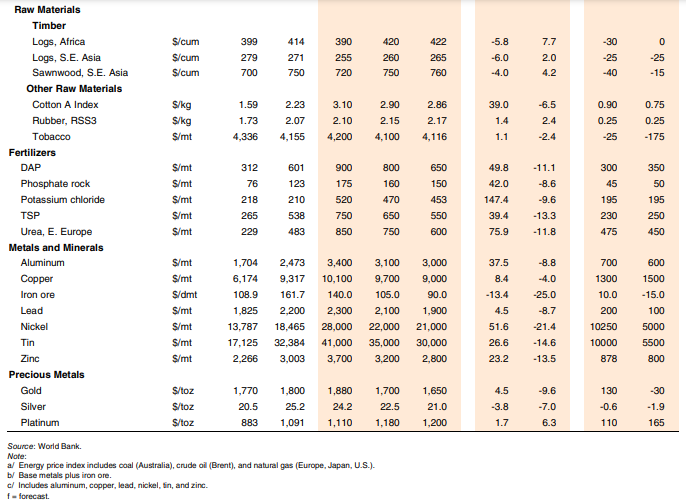

Commodity prices surged during the first quarter of 2022, reflecting the effects of the war in Ukraine as well as continued growth in demand and various constraints on supply (figure 1.A). Amid concerns about the war’s disruptive effects on commodity supply, the increases in prices were particularly pronounced for commodities where Russia and Ukraine are large exporters, particularly energy, fertilizers, and some grains and metals. These developments have added to a broad-based rise in commodity prices that began in mid-2020 with a surge in demand driven by receding concerns about the COVID-19 pandemic. Demand for commodities rebounded as the global economy recovered, while commodity production increased more slowly, weighed down by several years of weak investment in new production capacity as well as various supply disruptions. As a result, energy prices (in U.S. dollar terms) were more than four times higher in March 2022 than their April 2020 lows—the largest 23-month increase in energy prices since the 1973 oil price hike (figure 1.B). Fertilizer prices rose by 220 percent between April 2020 and March 2022, their largest 23-month increase since 2008 (figure 1.C). Similarly, food prices rose by 84 percent, their largest increase in a comparable period since 2008 (figure 1.D). These increases in prices are having major humanitarian and economic impacts and exacerbating food insecurity and inflation in many countries. Energy prices have increased sharply since the start of the year, with broad-based increases across all fuels; some coal and natural gas benchmarks reached all-time highs in March. Several countries, including Canada, the United Kingdom, and the United States announced sanctions on imports of Russian energy; some energy-producing companies announced they would cease operations in Russia; and many traders chose to discontinue trades in Russian oil, partly because of difficulties in obtaining insurance on cargoes or making transactions. Brent crude oil averaged $116/bbl in March 2022, an increase of 55 percent compared with December 2021. After rising to a 10-year high in early March, it eased in April following announcements of significant releases of oil from strategic inventories by the United States and other International Energy Agency (IEA) members, as well as expectations of weaker demand due to COVID-19-related lockdowns in several cities in China. Natural gas prices in Europe reached an all-time high in March, reflecting fears of disruption to imports from Russia. U.S. natural gas prices rose by almost a third in March relative to December 2021, in part reflecting increased demand for U.S. exports of liquefied natural gas. Coal prices also reached an all-time high in March due to increased demand for it as a substitute for natural gas in electricity generation. Most non-energy prices have risen since the start of 2022, with particularly large increases for fertilizers, nickel, oilseeds, and wheat. Among agricultural commodities, wheat prices saw a very steep increase, and were almost 30 percent higher in March compared to December 2021. Most edible oil prices have increased sharply this year, partly owing to production shortfalls in South America as well as disruptions to Ukraine’s sunflower seed oil exports. In contrast, rice prices saw only a modest increase, reflecting ample supplies in China and India. Fertilizer prices also increased sharply during 2022Q1, partly reflecting the surge in natural gas and coal prices, as both are key inputs into fertilizer production. The metals and minerals index rose 13 percent in 2022Q1 (q/q) and is now 24 percent higher than a year ago. Nickel prices rose 35 percent in the quarter, chiefly due to a short squeeze that led the London Metal Exchange to halt trading in the metal for several days in mid-March. Aluminum and iron ore prices also saw large increases, reflecting Russia’s importance in supply.

Outlook and risks

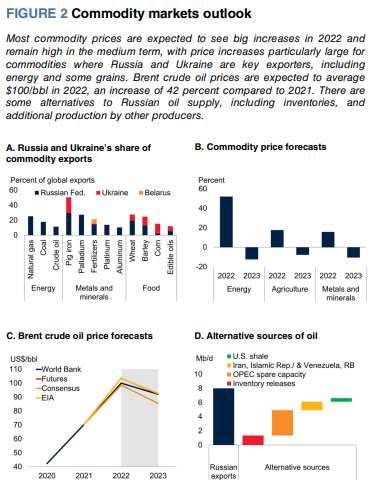

Commodity markets are facing an unprecedented array of pressures, lifting some prices to all-time highs, particularly for commodities where Russia or Ukraine is a key exporter (figure 2.A). These conditions may persist for three reasons. First, increased prices for one commodity typically induce substitution in demand toward other commodities, thereby alleviating the original price pressures. There is less scope for substitution today, however, because the increases in prices over the past year have been large and broadbased. For example, in the case of energy, crude oil is now one of the cheapest fuels per unit of energy, a notable difference from earlier energy price hikes when coal and natural gas were much cheaper. Second, the increases in prices of some commodities have pushed up the production costs of other commodities. For example, rising energy prices increase the cost of inputs to agriculture production, such as fuel and fertilizers. Similarly, increasing energy prices drive up the cost of extracting and refining metal ores, particularly for aluminum, iron ore, and steel. In turn, higher metal prices increase the cost of renewable energy technologies. The broader increase in inflation, globally, is also raising the costs of production of commodities, including through higher wages, higher transportation and storage costs, and, as interest rates increase, higher costs of borrowing.

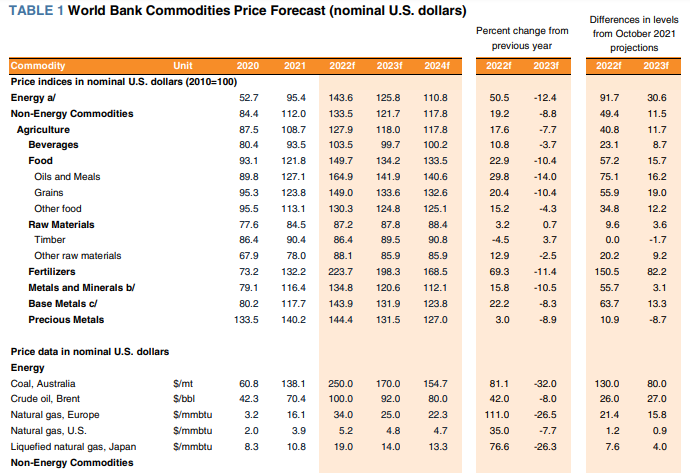

Third, many governments have responded to high fuel prices with tax cuts and subsidies. While these policies may somewhat alleviate the immediate impact of price hikes, they do not provide large benefits to vulnerable groups and may actually exacerbate the underlying issue by increasing energy demand. Most commodity prices are expected to be sharply higher in 2022 than in 2021 and to remain elevated in 2023-24 compared to their levels over the past five years (figure 2.B). Energy and nonenergy prices are forecast to rise by 50 and 20 percent in 2022, respectively, before pulling back somewhat in 2023 and settling at much higher levels than in the previous forecast. While the outlook for commodity markets depends heavily on the duration of the war in Ukraine and the extent of sanctions, it is assumed that the channels through which commodity markets have been affected are likely to persist. Changes in commodity trade patterns are expected to continue even after the war ends. The possibility of further outbreaks of COVID-19 in China, alongside a broader slowdown in global growth, present downside risks for prices. Among energy commodities, Brent crude oil prices are expected to average $100/bbl in 2022, an increase of 42 percent compared to 2021 (figure 2.C). Russia’s energy exports are expected to be severely disrupted as many countries seek alternative suppliers. Declining supply from Russia, however, is being partially offset by inventory releases and diversion of exports to other countries. Prices are expected to average $92/bbl in 2023 as supply disruptions ease and production rises outside Russia, while demand is likely to grow more slowly than previously expected. The disruptions resulting from the war are likely to have a lasting impact on Russia’s oil production due to the exit of foreign oil companies, weaker investment, and reduced access to foreign technology. Natural gas and coal prices are also expected to be significantly higher in 2022, with natural gas prices in Europe projected to be more than double their 2021 levels. Coal prices are forecast to average just over 80 percent higher in 2022 relative to 2021. As with crude oil, natural gas prices are expected to ease in 2023 as new supplies come on stream, including additional terminals for liquefied natural gas. Lower natural gas demand, and increased investment in renewable energy sources will also dampen prices. There is a material risk that energy prices could increase much more than forecast, especially if EU sanctions on Russian energy are broadened. This could lead to significant market disruptions.

While there is scope for some diversion of Russia’s energy exports to countries that are not imposing sanctions, these will be limited by the availability of infrastructure and involve higher transport costs. This is particularly the case for Russian natural gas, which is chiefly exported via pipelines to Europe. In the case of oil, there are some alternatives to Russian exports, including inventories and additional production by other producers (figure 2.D). However, there are concerns that OPEC spare capacity may be less than currently estimated, as evidenced by recently limited supply responses to increased prices. In addition, the U.S. shale industry faces constraints to significantly increasing output further, including shortages of labor and other inputs. Agricultural prices are forecast to rise by 18 percent this year, reflecting war-related supply disruptions in Ukraine and Russia and higher costs of inputs, including fuel, chemicals, and fertilizers. The war has already disrupted exports from Ukraine and will severely interrupt agricultural production in 2022, including production of maize, barley, and sunflower seed oil, which are typically planted in the spring. Also, in Russia, the lack of access to agricultural inputs, such as seeds and farm machinery, could reduce agricultural production. Accordingly, the projected 2022 increase in the agriculture price index reflects surges in wheat and maize prices. Agricultural prices are expected to fall back in 2023, reflecting increased supplies from the rest of the world, particularly wheat from Argentina, Brazil, and the United States. Nonetheless, agricultural prices in 2023-24 will remain well above previous forecasts, and could be subject to further upward pressures if input costs rise further. In particular, the sharp rise in fertilizer prices could lead to a reduction in their use, particularly in EMDEs, which could lower agricultural yields. Metal prices are projected to increase by about 16 percent in 2022 relative to 2021 and ease somewhat in 2023, while remaining at historically elevated levels. Nickel and aluminum prices are expected to increase by 52 and 38 percent, respectively, reflecting Russia’s outsize role as a supplier in these markets as well as the energyintensive nature of aluminum production. Upside risks to the price forecast relate to the possibility of worsening geopolitical tensions. On the downside, a prolonged period of lockdowns in China could reduce metal demand and hence prices.

Special Focus: The impact of the war in Ukraine on commodity markets

The war in Ukraine has been a major shock to global commodity markets. The supply of several commodities has been disrupted, leading to sharply higher prices, particularly for energy, fertilizers, and some grains. This Special Focus compares the current rise in prices with earlier oil and food price hikes in the 1970s and in 2008-09. Previous price hikes resulted in the emergence of new sources of supply for both oil and food. In the case of oil, price hikes also led to sustained reductions in demand as a result of substitution to other fuels and improvements in energy efficiency, facilitated by government policies. These episodes offer lessons for the current price hike. In the short term, supply disruptions and higher food and energy prices will raise inflation and policymakers will need to mitigate their impact on poorer households. The long-term effects of the war on commodity markets will depend on how extensively commodity trade is diverted, how much demand is reduced, and whether new supplies emerge. Policymakers can take action to accelerate structural changes that alleviate upward pressure on energy prices, including promoting energy efficiency and incentivizing new low-carbon sources of energy production. These policies would also protect economies from future energy price volatility and accelerate the transition away from fossil fuels, helping to achieve climate change goals. At present, however, many governments have focused on trade restrictions, price controls, and subsidies, which can be expensive and often exacerbate supply shortfalls and price pressures.

Source: worldbank.org