Energy prices continued to surge in the third quarter of 2021 while most non-energy prices plateaued following steep increases earlier in the year. After reaching all-time highs, natural gas and coal prices are expected to decline in 2022 as demand growth slows and supply constraints ease. Crude oil prices are forecast to average $74/bbl in 2022, up from a projected $70/bbl in 2021. After rising more than 48 percent this year, metal prices are projected to decline 5 percent in 2022. Agricultural prices are expected to broadly stabilize in 2022, following a 22 percent increase in 2021. High commodity prices, if sustained, could slow growth in energyimporting countries and exacerbate food insecurity in low-income countries. Risks to the forecast include adverse weather, further supply constraints, and new outbreaks of COVID-19. The fluctuations in commodity prices this year highlight some of the challenges in transitioning to a zero-carbon economy. Cities have a key role to play, given they account for around two-thirds of energy demand and greenhouse gas emissions. A special focus documents that urbanization is associated with increased commodity demand, but high-density cities can have lower per-capita commodity demand than low-density cities. This reinforces the need for strategic urban planning to minimize the impact of future urbanization on commodity demand.

Recent trends

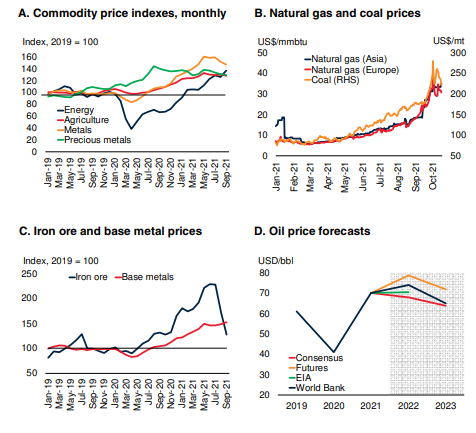

Energy prices rose sharply in 2021 Q3 while nonenergy prices plateaued (figure 1.A). Among the four major non-energy indexes, agriculture, fertilizers, and precious metals are about one-third above their pre-pandemic levels, while metals and minerals are around one-half higher. Adverse weather has buffeted many commodity markets: unusually high summer temperatures increased demand for electricity; droughts reduced hydroelectricity supply and affected some agricultural commodities, while floods impacted the supply of some metals and coal. Soaring natural gas and coal prices indirectly impacted production of other commodities, including fertilizers and some metals. Commodity markets have also been affected by the uneven recovery from the COVID-19 pandemic and supply chain disruptions.

Energy prices rose by 16 percent in 2021Q3 (q/q), continuing their upward trajectory since the start of the year, with natural gas and coal prices rising much faster than crude oil prices. Crude oil prices averaged $72/bbl in 2021Q3, an increase of 7 percent on the previous quarter, but with prices fluctuating significantly during the period. Prices initially softened in August amid worries about renewed outbreaks of the pandemic, but these were offset later in the quarter by supply disruptions in the U.S. arising from Hurricane Ida, as well as the broader rally in energy prices.

Natural gas prices rose by 69 percent in 2021Q3, and coal prices increased 44 percent, with some price benchmarks for both commodities reaching all-time highs (figure 1.B). The economic recovery (particularly in China) is largely behind the surge as it has boosted demand for fossil fuels for electricity generation. Unusually hot weather in some countries also boosted electricity demand for cooling. Furthermore, electricity production from renewable sources declined in several countries due to drought and low wind speeds.

Although non-energy prices were unchanged in 2021Q3 (q/q) as a group, there has been significant variation among commodities. The Metals and Minerals Price Index declined 1 percent in the quarter, with drops in iron ore (-17 percent) and copper (-3 percent) and gains in other base metals (9 percent) on average (figure 1.C). The sharp fall in iron ore prices was largely due to China’s reduction in steel production in order to meet zero-growth targets for the year. Demand for base metals has continued to increase, driven by the global economic recovery, while production has been disrupted by energy shortages and lockdowns. Precious metal prices fell 3 percent in 2021Q3 (q/q) amid a rise in U.S. 10-year Treasury yields, with larger falls for platinum (-13 percent) and silver (-9 percent) compared to gold (-1 percent). Platinum prices have been depressed by disruptions to car production globally, which have reduced demand for catalytic convertors.

FIGURE 1 Commodity market developments In 2021 Q3, energy prices rose sharply while many non-energy prices plateaued at high levels. Natural gas and coal prices soared amid high demand for electricity. Iron ore prices fell sharply from an all-time high as China reduced steel output; overall base metal prices continued to rise. Crude oil prices are expected to rise in 2022 before declining in 2023 as the recovery in demand is met by increased production. Looking ahead, the pattern of commodity demand will be affected by a continued increase in urbanization, with high-density cities having much lower energy use and CO2 emissions than low-density cities.

Agricultural commodity prices stabilized during 2021Q3, with declines in some food prices (e.g., rice) being offset by higher beverage prices (especially coffee). Despite tight supply conditions for some food commodities due to unfavorable weather (e.g., maize and soybeans), most food commodity markets remain adequately supplied by historical norms. However, the rally in energy prices, especially coal and natural gas, have sharply increased agricultural input costs. This includes fertilizers, which have risen more than 55 percent since January, with several fertilizer manufacturers halting or reducing production capacity. Elevated food prices combined with the recent spike in energy costs is pushing food price inflation up in several low-income countries (such as Ethiopia, Zambia, and Zimbabwe) as well as higher-income EMDEs, including Argentina and Turkey. High food prices may further exacerbate food insecurity—according to the Food and Agriculture Organization of the United Nations (FAO) and the World Food Programme (WFP)’s latest joint report, 23 low-income countries, including Ethiopia, Madagascar, and Somalia are facing acute food insecurity.

Outlook and risks

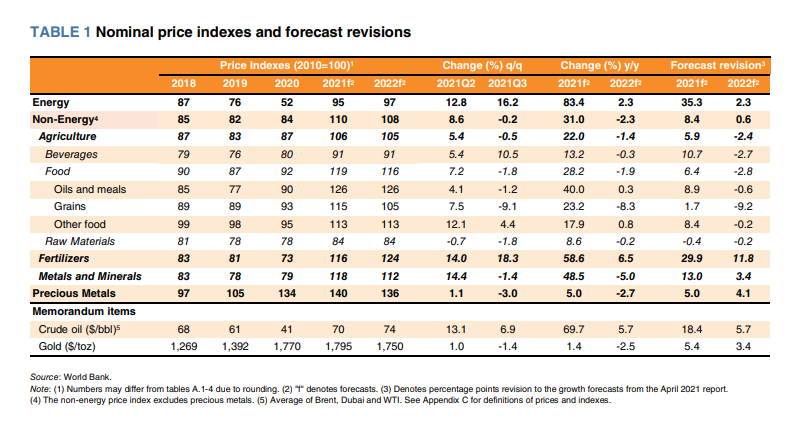

Energy prices are expected to increase more than 2 percent in 2022 after jumping more than 80 percent in 2021, supported by continued robust demand and gradual production gains, before falling sharply in 2023 as supply increases measurably (Table 1). Increasing energy prices pose significant inflation risks in many EMDEs and could weigh on growth in 2022 among energy-importing countries. Non-energy prices are projected to decrease somewhat in 2022 and 2023, with declines in both agriculture and metals prices as supply constraints ease.

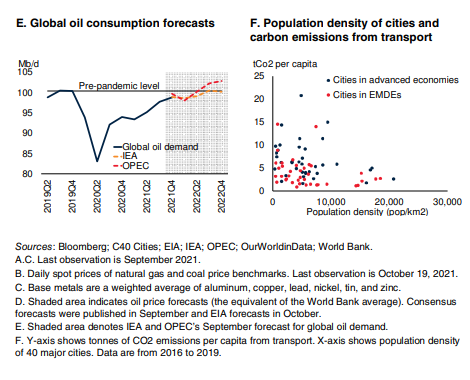

Oil prices are forecast to average $74/bbl in 2022, up from a projected $70/bbl in 2021, before dropping to $65/bbl in 2023. Oil demand is expected to continue its recovery and reach its prepandemic level by the second half of 2022. Oil production is expected to increase as supply outages are resolved; as production responds to higher demand, particularly shale production in the United States; and as OPEC and its partners unwind the rest of their production cuts. Investment shortfalls in new production, including U.S. shale, pose an upside risk. Investment in new oil production fell sharply in 2020 and has been slower to pick up than after previous price collapses. Furthermore, the substitution of crude oil for coal and natural gas in heating and electricity production poses another upside risk. Additional outbreaks of COVID-19 remain a downside risk to oil demand.

Natural gas and coal prices are expected to decline in 2022 and fall further in 2023, as demand growth eases (especially outside of Asia) and production and exports increase, driven by the United States. Further price spikes are likely, however, as inventories remain very low, and production is not expected to materially increase until 2022. More broadly, the events of this year have highlighted how changing weather patterns due to climate change are a growing risk to energy markets, affecting both demand and supply. From an energy transition perspective, concerns about the intermittent nature of renewable energy highlight the need for reliable baseload and backup electricity generation. These will increasingly need to be from low-carbon sources, such as hydropower or nuclear power, or from new or better methods of storing renewable power. At the same time, the surge in natural gas and coal prices this year has made solar and wind power more competitive as an alternative energy source. Countries can benefit from accelerating the installation and transmission of renewable energy and reducing their dependency on fossil fuels.

Metal prices are forecast to fall 5 percent in 2022 following a projected increase of 48 percent in 2021 as the global recovery eases and supply disruptions are addressed. Bottlenecks in the supply chain are not expected to be fully resolved until the end of 2022, as energy and shipping shortages take time to normalize. Key risks to the metal price forecast are the outlook for China’s property sector and energy-related supply disruptions.

Agricultural prices are expected to decline modestly in 2022 and 2023, following a projected 22 percent increase in 2021, as supply conditions improve. Upside risks to agricultural prices include high input prices, especially fertilizers, and more diversion of food commodities to the production of biofuels linked to efforts to decarbonize the global economy. High food prices have raised concerns about food insecurity in several EMDEs. In addition to lower incomes due to pandemic-driven production disruptions, several food-importing EMDEs are facing high international food prices and energy costs. According to the latest joint assessment by the Food and Agriculture Organization (FAO) and the World Food Program (WFP), food insecurity, which affected 155 million people in 2020 (up from 135 million in 2019), is expected to become more acute, with more than 41 million people worldwide being at risk of falling into famine or famine-like conditions.

Special Focus: Urbanization and commodity demand

The sharp fluctuations in energy prices observed this year highlight the difficulties in transitioning to a zero-carbon economy. Cities are on the frontlines of the energy transition; although they occupy less than 3 percent of global land, they consume over two-thirds of the world’s energy and account for a similar share of global greenhouse gas (GHG) emissions. The past 50 years have seen a rapid increase in urbanization rates globally, and this trend is set to continue over the next three decades. This edition of the Commodity Markets Outlook features a Special Focus on the linkages between urbanization and commodity demand. Mechanisms between urbanization and commodity demand include transport use in urban areas, household size and type of accommodation, the provision of infrastructure, and consumer preferences. After controlling for income and population, an increase in the share of the population living in urban areas is typically associated with higher energy consumption. However, high-density cities, especially in advanced economies, tend to have lower per capita energy consumption and lower GHG emissions from transport than less densely populated cities (figure 1.F). For policymakers, this reinforces the importance of strategic planning and high-quality infrastructure, particularly for transport, in limiting the impact of urbanization on commodity consumption while also boosting the quality of life in cities.

Source: worldbank.org