A sharp global growth slowdown and concerns about an impending global recession are weighing on commodity prices. In many economies, however, prices in domestic-currency terms remain elevated because of currency depreciations. This could deepen the food and energy crises already underway in a number of countries. As the global growth slowdown intensifies, commodity prices are expected to ease in the next two years, but they will remain considerably above their average over the past five years. Energy prices are expected to fall by 11 percent in 2023 and 12 percent in 2024. Agricultural and metal prices are projected to decline 5 and 15 percent, respectively, in 2023 before stabilizing in 2024. This outlook, however, is subject to numerous risks both in the short- and medium-term. Energy markets face an array of supply concerns as worries about the availability of energy during the upcoming winter intensify in Europe. Higher-than-expected energy prices could pass through to non-energy prices, especially food, prolonging challenges associated with food insecurity. A sharper slowdown in global growth presents a key downside risk, especially for crude oil and metal prices. A Special Focus section suggests that concerns about a possible global recession have already contributed to a decline in copper prices from their peak in March 2022, and a shift in demand from aluminum has contributed to lower aluminum prices. Prices will likely remain volatile as the energy transition unfolds and demand moves from fossil fuels to renewables, which will benefit some metal producers. Metal-exporting countries can make the most of the resulting opportunities for growth over the medium-term, while limiting the impact of price volatility by ensuring they have well-designed fiscal and monetary frameworks.

Recent trends

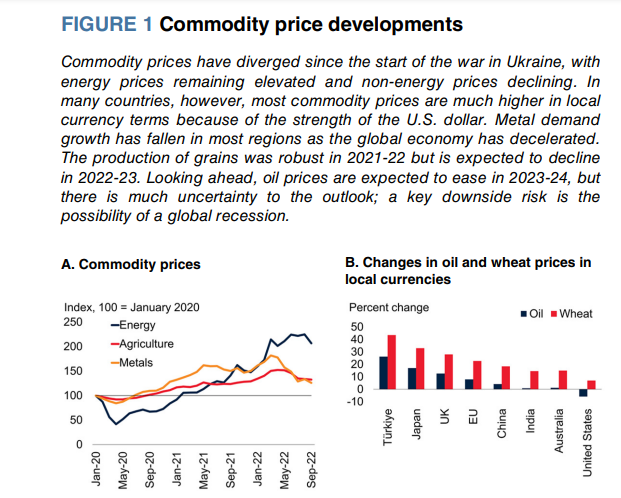

Most commodity prices have retreated from their peaks in the aftermath of the post-pandemic demand surge and war in Ukraine as global growth slows and worries about a global recession intensify. However, individual commodities have seen divergent trends amid differences in supply conditions and their response to softening demand (figure 1.A). Moreover, currency depreciations in many countries have resulted in higher commodity prices in local currency terms compared to the price in U.S. dollars (figure 1.B).

For example, from February 2022 to September 2022, the price of Brent crude oil in U.S. dollars fell nearly 6 percent. Yet, because of currency depreciations, almost 60 percent of oil-importing emerging market and developing economies saw an increase in domestic-currency oil prices during this period. Nearly 90 percent of these economies also saw a larger increase in wheat prices in localcurrency terms compared to the rise in U.S. dollars. As a result, commodity-driven inflationary pressures in many countries with depreciating currencies may be more persistent than indicated by recent declines in global commodity prices. /is could prolong the food and energy crises already affecting many developing economies.

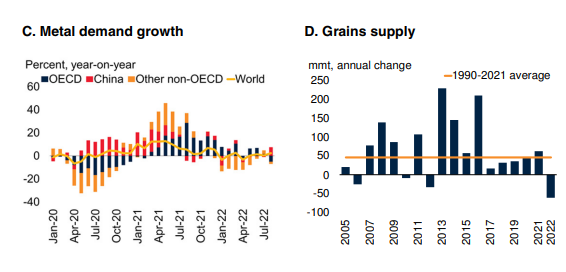

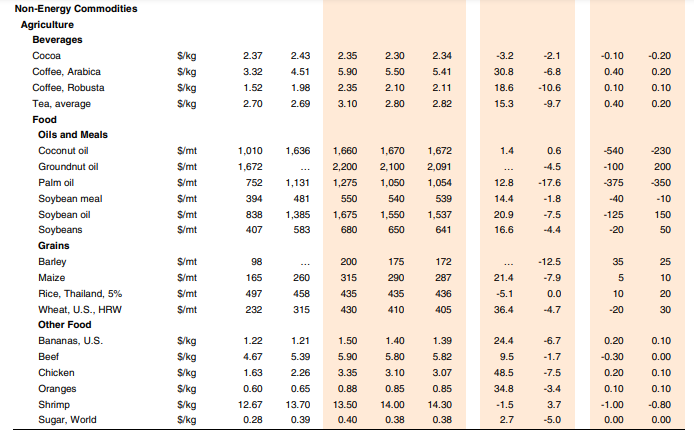

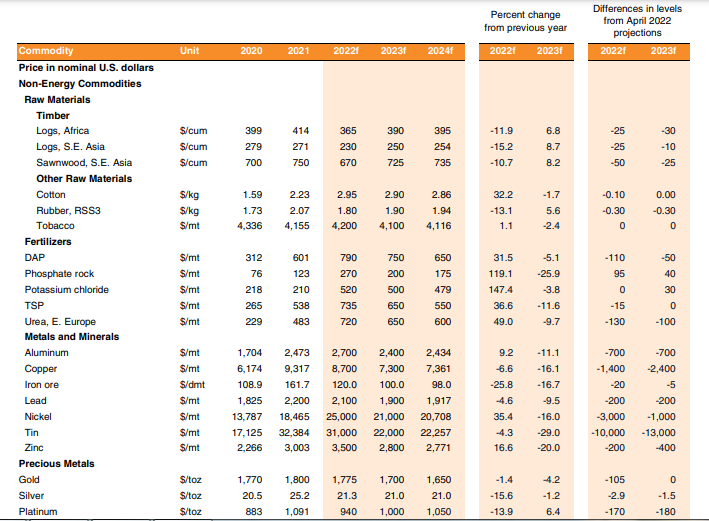

Energy prices have diverged widely and have been extremely volatile since the outbreak of the war in Ukraine. Brent crude oil prices fell sharply during 2022Q3 (nearly one-quarter lower in September 2022 relative to its June 2022 peak) due to concerns about a global recession in 2023 and tightening financing conditions. Prices partially rebounded in October following the announcement by OPEC+ members on October 5th to reduce their production target by 2 million barrels per day (mb/d) but have been volatile since. Natural gas prices in Europe reached all-time highs in August 2022 due to aggressive actions by several countries to rebuild their inventories as well as reduced flows of gas from Russia. Prices have since dropped sharply as inventories reached their target levels and demand has fallen. Coal prices continued to increase in 2022Q3, as many countries turned to coal as a substitute for natural gas. During the past four quarters, natural gas prices in Europe and seaborne coal prices have averaged 420 and 180 percent higher, respectively, than their average over the past five years. Non-energy prices declined 13 percent in 2022Q3 (q/q). Metal prices declined the most, largely reflecting weaker global growth and concerns about a slowdown in China (figure 1.C). Precious metal prices fell 9 percent (q/q) as global interest rates rose sharply. Agricultural commodity prices fell 11 percent in 2022Q3 (q/q). Fears about food shortages earlier in the year gradually eased. Exports from Ukraine restarted and inventories of key crops remain above historical levels, thereby providing a buffer for the ongoing 2022-23 season. Notwithstanding the decline in agricultural commodity prices from their March 2022 highs, they remain nearly 9 percent higher than a year ago. Expected supply shortfalls in the current season for some key commodities, especially maize, coupled with adverse weather and high energy prices, could keep prices high during the current season (figure 1.D).

Outlook and risks

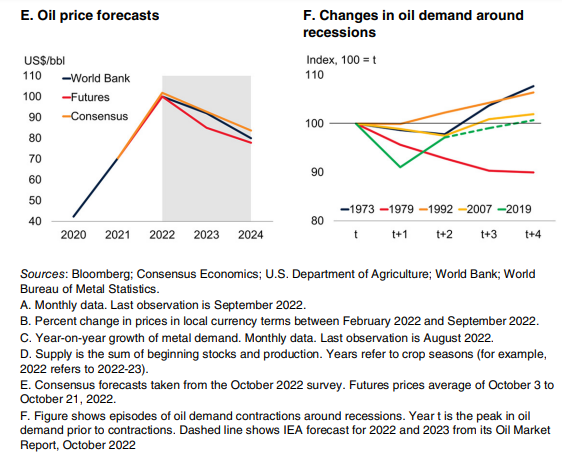

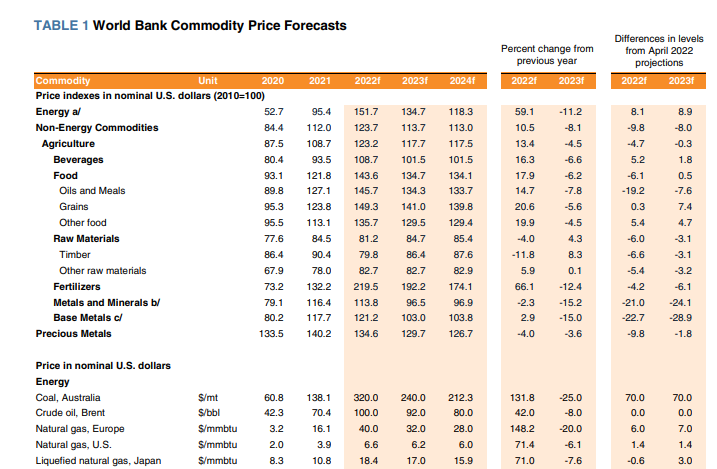

After surging by an expected 60 percent in 2022, energy prices are projected to decline 11 percent in 2023 and a further 12 percent in 2024. Key drivers of the outlook include slower global growth, weaker demand for natural gas as households and industry reduce consumption, and some supply responses, primarily for coal. However, prices will remain more than 50 percent above their five-year average through 2024. Persistently high energy prices will continue to have inflationary implications, particularly through second-round effects such as higher transport and electricity costs for businesses. Inflationary pressures stemming from commodity prices will be further exacerbated in countries that have had sizeable currency depreciations against the U.S. dollar. Brent crude oil prices are forecast to average $92/ bbl in 2023, down from a projected $100/bbl in 2022, before easing to $80/bbl in 2024 (Figure 1.E). Oil consumption is expected to continue to increase by just under 2 percent in 2023 as China gradually reopens, and as switching from natural gas to oil continues, especially in electricity generation. A sharper-than-expected slowdown in global growth and continued COVID restrictions in China are the key downside risks to oil consumption. During previous global recessions oil demand has declined by about 2 percent in the first year and 1 percent in the second, although with wide variation (figure 1.F).

Oil markets are expected to tighten over the next few months as additional sanctions restrict exports from Russia, releases of oil from strategic reserves in several countries come to an end, and as OPEC+ members cut production (even if somewhat less than the announced 2 mb/d since many of the OPEC+ members are already producing below quota). This will more than offset the effect of rising production in a few countries, primarily the United States. The outlook is subject to numerous risks, especially on the supply side. First, production in the United States could disappoint as producers prioritize returning cash to shareholders over increasing output, and higher input costs constrain new investment. Second, the outlook for Russia’s production depends on the impact of trade measures. Russia’s exports next year could be as much as 2 mb/d lower, as the EU embargo on Russian oil and oil products (as well as restrictions on access to EU insurance and shipping services) comes into effect. The proposed G7 oil price cap could affect the flow of oil from Russia, but it is an untested mechanism and would need the participation of large emerging market and developing economies to achieve its objectives. Third, releases of crude oil from strategic reserves, including the U.S. are due to end this year; while these could be extended further, it would risk leaving strategic inventories at very low levels. Amid low levels of inventories, limited spare production capacity, and ongoing geopolitical events, the oil market is susceptible to price spikes. The materialization of some of these risks could intensify challenges associated with energy security in many countries. Natural gas and coal prices are also expected to ease in 2023 and 2024 but remain at much higher levels than their pre-pandemic averages. By 2024, Australian coal and U.S. natural gas prices are expected to be double their average over the past five years, while European natural gas prices could be four times higher. The expected easing of prices next year is due to weaker demand for natural gas as households and industries curtail their consumption and switch to substitutes, while coal production is expected to increase as China, India, and seaborne exporters boost output. The nearterm outlook for natural gas and coal prices will depend heavily on the severity of the winter in Europe. As with crude oil, slower global growth is a key downside risk to the outlook for next year. Concerns about energy shortages, particularly in Europe, will require careful policy coordination among key importers to ensure the burden of high energy prices, or future energy disruptions, is equitably shared. Recent government policy announcements to sharply increase the installation of renewable energy and reduce overall energy consumption may feed through into lower energy prices, but this will take time, and a worsening supply outlook in the winter of 2023 is possible. Furthermore, the current high inflation and highinterest rate environment will make financing investment in new energy production (both fossil fuels and renewables) more challenging, even if recent declines in metal prices provide some reduction in project costs. In the longer term, the prospect of persistently high energy prices may require a shift in industrial models in Northern European countries that have historically relied on natural gas imports by pipeline. Indeed, high energy prices have already led to the closure of some facilities in energyintensive industries, including fertilizer and chemical plants, as well as shifts in manufacturing patterns in others. Together, these changes should lead to reduced carbon emissions from the EU and may help accelerate its energy transition. In other countries, however, the implications for carbon emissions are less clear. A reduction in carbon intensity globally, not simply a shift in activities between countries, is needed to achieve climate change objectives. Following an estimated decline of nearly 2 percent, metal prices are forecast to fall more than 15 percent in 2023 before stabilizing in 2024. The weakness reflects the deterioration of global growth prospects along with China’s softening demand (due to its zero COVID policy and the slowdown of its real estate sector). Risks to the short-term outlook for metals are on the downside and reflect slower-than-expected global growth and a further deterioration of China’s property sector. One upside risk is higher-than-expected energy prices which could lead to increased production costs for metal refiners. In the longer term, however, metal demand is expected to increase, stimulated by recent government policies to accelerate the energy transition and boost renewables, which are metals intensive. Agricultural prices are forecast to decline by 5 percent in 2023 before stabilizing in 2024. The projected decline in 2023 reflects a better-thanexpected global wheat crop, stable supplies in the rice market, and the resumption of grain exports from Ukraine (although the maize crop is expected to contract materially during the 2022-23 season). However, there are numerous upside risks to the price forecast. First, disruptions in exports from Ukraine or Russia, both key grain exporters, could once again interrupt global supplies, as they did in the early stages of the war in Ukraine. Second, further increases in energy prices or disruptions in energy supplies (especially natural gas and coal, which are key inputs to fertilizers) could exert upward pressure on grain and edible oil prices. Third, adverse weather patterns can reduce yields; indeed, 2023 is likely to be the third La Niña year in a row, potentially reducing yields of key crops in South America and Southern Africa. On the downside, weaker-than-expected growth, especially in China, could affect the prices of certain agricultural commodities such as maize and soybeans, which are used as animal feed. As a result of developments in food markets following the Russian invasion of Ukraine, the number of people subject to severe food insecurity is projected to exceed 200 million in 2022. Populations facing food crises are typically in countries with conflict or countries that are facing extreme weather events, especially in Sub-Saharan Africa. Materialization of the upside risks to food prices outlined above could result in even larger increases in the number of people suffering from food insecurity.

Special Focus. Pandemic, war, recession: Drivers of aluminum and copper prices

Over the past three years, the pandemic, the war in Ukraine, and concerns about an impending global recession caused large swings in prices of aluminum and copper. Record price rebounds from pandemic lows in April 2020 were followed by renewed steep declines starting in March 2022. The price rebound after the pandemic was mainly driven by the economic recovery but, in contrast to the increase in prices after the global financial crisis, supply factors also contributed about onequarter to the rebound. Since March 2022, a steep global growth slowdown, an unwinding of supply constraints, and concerns about an imminent global recession (especially for copper) contributed to the plunge in prices. Prices will likely remain volatile as the energy transition unfolds and as global commodity demand shifts from fossil fuels to renewables, which are metals intensive. For metal-exporting countries, the energy transition may bring windfalls, but it could also increase their exposure to price volatility. In this regard, policymakers need to design strong fiscal and monetary frameworks now—and foster an environment for diversification—to make the most of the resulting opportunities for growth while limiting the impact of price volatility.

Source: worldbank.org